This article originally appeared in the October/November 2020 issue of the Deep-sea Mining Observer. It is reprinted here with permission. For the latest news and analysis about the development of the deep-sea mining industry, subscribe to DSM Observer here: http://dsmobserver.com/subscribe/

For the last decade, next-generation batteries have been the motivating force for the deep-sea mining industry. The electrification of the world’s vehicle fleets to wean society off of fossil fuels has created huge demands for cobalt, nickel, and other metals necessary for high-density batteries. The demand has placed the green revolution in a position where we either need to unlock new reserves of these essential metals or fundamentally change how we make batteries.

While new battery technologies promise to reduce or eliminate the need for cobalt and other metals, unlocking the raw materials needed to energize electric vehicles isn’t the only mineral supply chain that can support commercial exploitation of the deep seafloor. The critical minerals found in polymetallic nodules, seafloor massive sulphides, and cobalt-rich ferromanganese crusts are being eyed for a variety of production needs, both commercial and strategic.

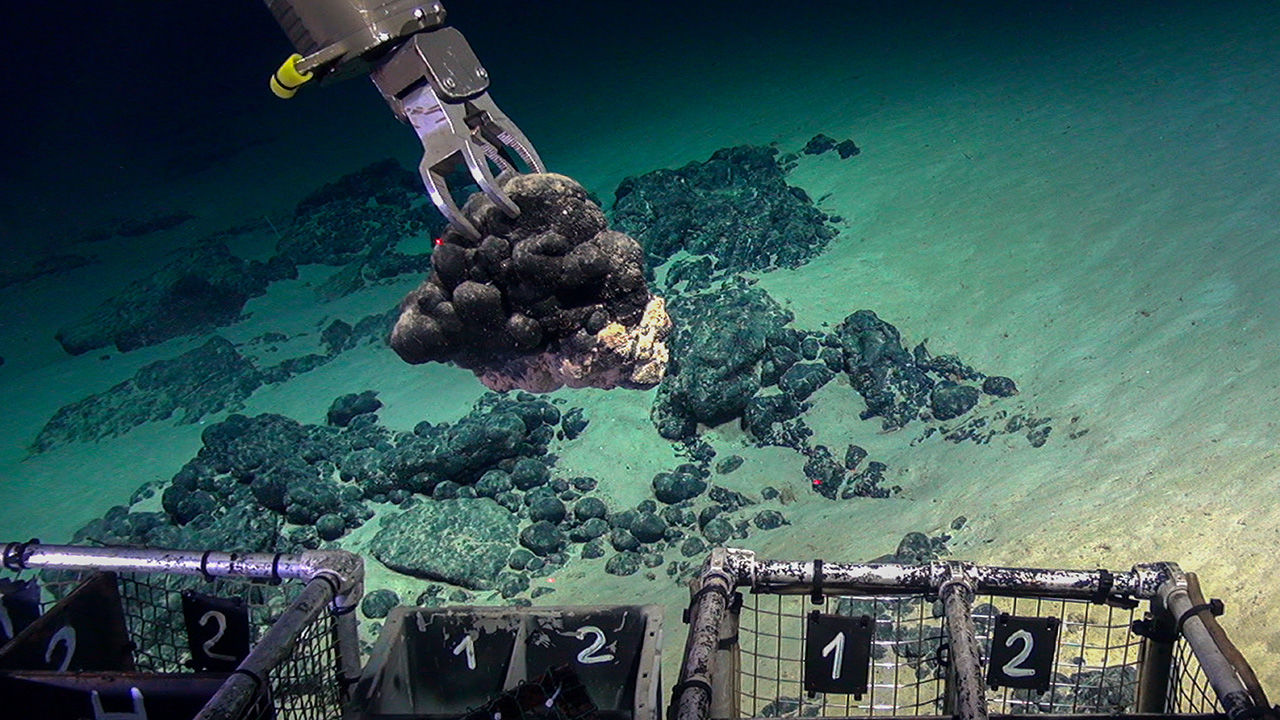

It was the manganese content of polymetallic nodules that originally caught the eye of prospectors in the 1960s and 1970s looking to exploit the mineral wealth of the deep oceans. Useful in the creation of steel and aluminum alloys, as well as a lead replacement in internal combustion engines, and as an electron acceptor in dry cell batteries, among other uses, the market for manganese crashed in the 1980s as more accessible sources came online and alternative technologies mitigated its demand. As the 12th most abundant element in the Earth’s crust, global manganese production more than satisfied demand. Since 2000, manganese has been used as a substitute for copper and nickel in several US coins.

But manganese and cobalt aren’t the only metal that occurs in abundance beneath the waves. Gold, nickel, copper, and rare earth elements are also commonly cited as viable resources to justify exploitation in areas beyond national jurisdiction. Two metals that aren’t quite as frequently discussed but may, nevertheless, prove attractive to deep-sea mining contractors, are scandium and tellurium.

Scandium is a particularly challenging resource. It is used to produce strong, lightweight aluminium alloys for aerospace components, as well as, in much lower quantities, in the manufacture of some sporting equipment and firearms. Only a handful of scandium operations exist, producing 15 to 20 tons of scandium per year as a byproduct of other mineral extraction. This represents about half the global demand, creating a powerful incentive to develop new and novel scandium prospects.

Scandium occurs in uniquely high quantities in polymetallic nodules and ferromanganese crust off the northern coasts of Alaska within the United States Exclusive Economic Zone. Scandium is also found in metal enriched muds in the northwestern Pacific Ocean, within Japan’s Exclusive Economic Zone associated with Minamitorishima Island. Much like other deep-sea elements, scandium, and its applications in making lightweight, energy efficient aircraft, makes it potentially an important component of the green revolution.

Tellurium is one of the rarest metals on Earth. It is a technology-critical element–it is extremely important for the development of emerging technologies. Tellurium is used in the production of semiconductors, fiber optic cables, and solar panels, among other uses. It is produced as a byproduct in copper and lead refining and is produced primarily within the United States, Japan, Canada, and Peru. A little more than 100 tons of tellurium are produced every year.

Most critically, tellurium is a key component of cadmium telluride solar cells; efficient, thin film solar cells which are more efficient at absorbing light than silicon-based solar cells. Cadmium telluride solar panels are cheaper per kilowatt than conventional silicon panels and are lighter and easier to deploy. Tellurium occurs in abundance in mineral-rich crusts of the Tropic Seamount, a mountain in the middle of the Atlantic, just south of the Canary Islands. The deposits on this seamount, which is alternately claimed to fall within the EEZs of both Spain and Morocco, may be 50,000 times richer than all terrestrial sources.

Scandium and tellurium are the oddball metals in the push to mine the deep-sea. While elements like cobalt, nickel, and copper are needed in massive quantities to supply an exploding demand for next-generation batteries, neither scandium nor tellurium production is needed at that scale. Their relative rarity and the novelty of their occurrence in a few deposits on the seafloor creates a much different value proposition for these resources. As critical minerals with sparse terrestrial sources, barring a future surge in demand, accessing seafloor deposits represents a strategic, rather than purely commercial, decision.

Scandium demand, in particular, could finally mark the long-expected return of the United States to the deep-sea mining industry.